carried interest tax concession

Given tax treatment is one of the key factors influencing the choice of jurisdiction for fund domiciliation and operations it is announced in the 2020- 21 Budget Speech that the Government plans to provide tax concession for carried interest distributed by PE funds operating in Hong Kong. Following its proposal to introduce a concessionary tax rate for carried interest earned from Hong Kong private equity funds on January 4 2021 the Hong Kong Government announced that eligible carried interest will be charged at a profits tax rate of 0 and that 100 of eligible carried interest will be excluded.

2

Received a preferred return at an annual rate of 6 compound interest that would also be considered carried interest.

. Qualifying carried interest broadly includes carried interest received from gains from investments in private companies. Tax concession rate The Proposal provides that eligible carried interest would be charged at a 0 profits tax rate such rate was kept silent under the Consultation Paper. 11 rows As part of a longstanding Government policy to attract private equity PE and investment fund.

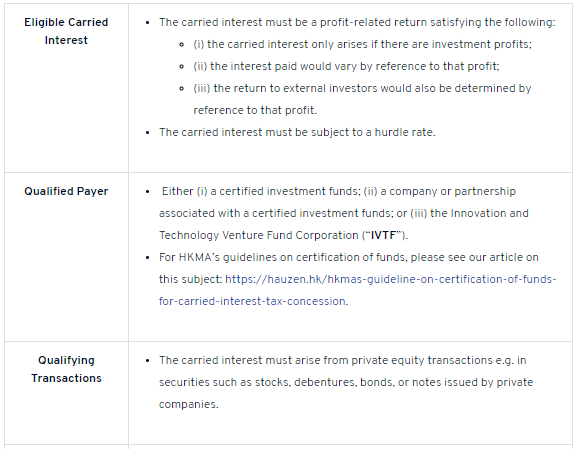

Carried interest tax concession - conditions Must be paid by a qualifying payer The carried interest must be paid by a certified investment fund ie. The concessional tax treatment for carried interest is now effective from 1 April 2020 and will provide for a 0 tax rate for qualifying carried interest. The legislative council brief accompanying the Bill specifies that carried interest derived from a hedging transaction may only be eligible for the Tax Concession if the hedging transaction forms part and parcel of the private equity transaction and the profits on the hedging transaction are embedded in the profits or loss on such transaction for the calculation of.

The Inland Revenue Amendment Tax Concessions for Carried Interest Ordinance 2021 Ordinance was enacted into law on 7 May 2021 by way of amendment to the Inland Revenue Ordinance IRO. For carried interest to qualify for the concession the underlying investments from which the carried interest is distributed must also comply with the same conditions governing exemption from tax. Under this new concession eligible carried interest received or accrued on or after from 1 April 2020 will be subject to zero percent profits tax.

As a prerequisite to the concessionary tax regime the eligible carried interest must arise from profits on the in-scope transactions 2 of private equity PE funds which are exempt from profits tax under the Unified Fund Exemption Regime UFR. Hong Kong Tax Incentive for. At the meeting of the Executive Council on 26 January 2021 the Council ADVISEDand the Chief Executive ORDEREDthat the Inland Revenue Amendment Tax Concessions for Carried Interest Bill 2021 the Bill at Annex A should be introduced into the Legislative Council LegCo to.

After six months of consultation the Inland Revenue Amendment Tax Concessions for Carried Interest Bill 2021 Bill providing for a tax concession for a 0 profits tax rate on eligible. 100 Exclusion for Salaries Tax eligible carried interest shall be fully excluded. Applying retrospectively to tax years commencing on or after 1 April 2020 the Amendment Ordinance has essentially transformed Hong Kong into one of the most tax efficient jurisdictions for fund.

Eligible Carried Interest will be taxed at 0 profits tax rate. Only carried interest distributed out of tax-exempted qualifying transactions in private equity investments ie shares stocks debentures loan stocks funds bonds or notes of or issued by a private company under Schedule 16C of the Inland Revenue Ordinance would be eligible for the tax concession. The Government has spared no efforts in developing Hong Kong as a premier PE fund hub.

The Inland Revenue Amendment Tax Concessions for Carried Interest Ordinance 2021 Ordinance was enacted into law on 7 May 2021 by way of amendment to the Inland Revenue Ordinance IRO. Specifically the carried interest must arise from a tax-exempted qualifying transaction in the shares stocks. To qualify for the tax concession the fund must be validated by the HKMA.

On 7 May 2021 the Inland Revenue Amendment Tax Concessions for Carried Interest Ordinance came into operation introducing the much-anticipated Carried Interest Tax Concession Regime the Regime. 0 Tax Rate for Profits Tax a qualifying person can enjoy concessionary tax rate of 0 on eligible carried interest received from a qualifying payer subject to certain conditions. Qualifying carried interest broadly includes carried interest received from gains from investments in private.

These include being a qualified recipient the need to comply with headcount and operating expenditure substance requirements as well as the need for the fund be certified by the Hong Kong Monetary Authority and the Inland Revenue. January 11 2021. Under this new concession eligible carried interest received or accrued on or after from 1 April 2020 will be subject to zero percent profits tax.

The tax concession involves a number of conditions that must be satisfied for a carried interest to qualify for the concession. On 7 May 2021 the Inland Revenue Amendment Tax Concessions for Carried Interest Ordinance 2021 the Amendment Ordinance was enacted into law. Eligible carried interest recipients.

Asset Management Tax Update of 29 January 2021 provided an overview of the Carried Interest Tax Concession Bill. The proposal states that the tax concession only applies to carried interest distributed by PE transactions only. A qualifying payer is any of the following.

Furthermore the Proposal clarifies that 100 of eligible carried interest would also be excluded from the employment income for the calculation of the investment professionals salaries tax. With some expectation a gain on an investment in a public company or from any other non. Inland Revenue Amendment Tax Concessions for Carried Interest Bill 2021.

The Regime operates to provide tax concession at both the salaries tax and profits tax levels. The concessional tax treatment for carried interest is now effective from 1 April 2020 and will provide for a 0 tax rate for qualifying carried interest. That is where an entity that is recipient of the carried interest return pays part of the return to its employees that payment will be concessionally taxed.

The tax concession for a carried interest also looks through to the employees.

Ey Avcj Asia Cfo Coo Forum

Asset Management Update Kpmg China

Carried Interest Tax Concession Regime For Private Equity Funds Lexology

The Hong Kong Limited Partnership Fund Explained

Asset Management Tax Update Kpmg China

Pwc Cn Publication More Good News Carried Interest Tax Concession

Pwc Cn Publication New Year Good News Carried Interest Tax Concession

A New Era For Carried Interest In Hong Kong Kpmg China

2

Introduction Of Carried Interest Tax Concessions For Hong Kong Private Equity Funds

Hong Kong S Carried Interest Tax Concession Zero Tax Insights Proskauer Rose Llp

Hong Kong S Tax Concession For Carried Interest Getting Funds Certified With The Hkma

Pwc Cn Publication New Year Good News Carried Interest Tax Concession

Proposal On Hong Kong S Carried Interest Tax Concession Regime Lexology

Dentons Hong Kong Carried Interest Tax Concessions For Private Equity Fund Operators In Hong Kong Enacted As Law Retrospective Effect From April 2020

Asset Management Tax Update Kpmg China

New Tax Breaks A Magnet For Private Equity Funds The Standard

Introduction Of Carried Interest Tax Concessions For Hong Kong Private Equity Funds

Introduction Of Carried Interest Tax Concessions For Hong Kong Private Equity Funds